Valuing Shares With Earnings

Right now, we’ll enterprise somewhat into the basic evaluation nook, and we provides you with a glimpse of an intriguing paper (Hillenbrand and McCarthy, 2024) that discusses some great benefits of utilizing ‘Road’ earnings over conventional GAAP earnings. The paper means that ‘Road’ earnings present higher valuation estimates and improved monetary evaluation. Is that this a means the way to enhance the efficiency of the struggling fairness worth issue?

Road earnings comprise extra details about future fundamentals than GAAP earnings as a result of they exclude transitory objects. In addition they don’t endure from points with smoothing previous earnings and are unaffected by shifts in company payout insurance policies. When making use of the Campbell-Shiller decomposition to the Road price-earnings ratio, the outcomes align with the surplus volatility puzzle (Shiller, 1981): fluctuations within the Road price-earnings ratio are primarily pushed by future returns, with little rationalization from future earnings development.

This implies that inventory returns ought to exhibit predictable return variation, a significant implication of the surplus volatility puzzle. Accordingly, they reveal that the Road price-earnings ratio can predict inventory returns each in-sample and out-of-sample. Their findings point out that the Road price-earnings ratio is good for finding out the surplus volatility puzzle and return predictability. It might additionally assist traders time their market publicity extra successfully.

Regardless of the potential subjectivity, it’s proven in Determine 3 that mixture “earnings can carefully replicate mixture Road earnings reported by I/B/E/S earlier than particular objects” utilizing Compustat. This suggests that subjectivity doesn’t play a big position since we will replicate the earnings numbers following a hard and fast algorithm.

An open query stays as to what drives extreme inventory value actions. The road price-earnings ratio reveals traders’ expectations of returns and earnings will help clarify the surplus volatility puzzle.

Authors: Sebastian Hillenbrand and Odhrain McCarthy

Title: Valuing Shares With Earnings

Hyperlink: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4892475

Summary:

To handle the surplus volatility puzzle – the extreme actions in inventory costs – researchers usually examine actions in valuation ratios. Nonetheless, we reveal that actions in valuation ratios primarily based on basic measures with excessive transitory volatility, corresponding to generally used earnings measures, are uninformative about actions in inventory costs. To beat this, we suggest utilizing another basic measure: Road earnings. Road earnings, calculated earlier than numerous transitory objects, don’t possess this transitory volatility and supply a extra informative measure of future fundamentals. Consequently, actions within the price-to-street earnings (Road PE) ratio replicate actions in inventory costs, making it extremely informative in regards to the extra volatility puzzle. Accordingly, we present that the Road PE has extra in- and out-of-sample explanatory energy for predicting returns than different valuation ratios. Moreover, it helps reconcile conflicting views on which subjective expectations drive inventory value actions, displaying that expectations of short-term earnings development, long-term earnings development, and returns can all assist clarify the surplus volatility puzzle.

As all the time, we current a number of thrilling figures and tables:

Notable quotations from the educational analysis paper:

“To validate the usage of Road earnings, we reveal that, on the mixture stage, Road earnings are certainly a extra steady and informative measure of earnings than GAAP earnings. First, we present the massive distinction between mixture Road and GAAP earnings arises because of earnings assertion objects categorised as “particular objects”. Particularly, mixture (and industry-level) Road earnings (from I/B/E/S) are carefully replicated by computing mixture (and industry-level) earnings earlier than “particular objects” as reported in Compustat.2 Second, as a result of particular objects correspond to transitory objects (corresponding to one-off impairments, write-downs, and many others.), by eradicating these transitory objects, Road earnings are smoother and extra persistent than GAAP earnings. Third, as a result of transitory objects have little relevance for future earnings, previous Road earnings are extra informative about future mixture earnings (each GAAP and Road), in line with the firm-level proof documented in Rouen, So, and Wang (2021).

Utilizing the Road PE, we discover statistically and economically vital proof for in-sample return predictability, for each brief and long-horizon returns. The bias-adjusted predictive coefficients of −0.68 (p = 0.067), −2.43 (p = 0.021), and −4.95 (p = 0.005) for 1-year, 3-year, and 5-year returns, respectively, point out vital predictive energy. The growing magnitude of those coefficients over longer horizons not solely helps theories of imply reversion in anticipated returns (Fama and French, 1988; Campbell, 2001), but in addition supplies sturdy proof that actions within the Road PE are intimately linked to long-run returns. For instance, a one-point enhance within the Road PE predicts almost a 5% lower in returns over the subsequent 5 years. On condition that Road PE ranges from 7 to twenty-eight, this implies that when shares are at their most cost-effective, anticipated returns over the subsequent 5 years are roughly 105% larger than when they’re at their most costly. Comparable outcomes are noticed when utilizing the 3-year Road PE. The Road PE constantly outperforms different valuation ratios – PD, CAPE, and GAAP PE – in predictive energy for returns. In reality, not one of the conventional measures are vital on the 5% stage for the 1-year or 3-year horizon, and solely the PD is important on the 5% stage for the 5-year horizon.

We conclude that the variation in future returns induced by extra inventory value actions can certainly be predicted utilizing the Road PE. Thus, utilizing the Road PE ratio reconciles return predictability check swith the surplus volatility puzzle. Our return predictability proof is all of the extra exceptional because it reveals strong in- and out-of-sample pattern predictive energy with out counting on “theory-motivated” regression frameworks (e.g., Lewellen, 2004; Cochrane, 2008; Campbell and Thompson, 2008) or complicated estimation methods (e.g., Kelly, Malamud, and Zhou, 2024).3

[Authors] examine paperwork that Road earnings are basic measure for valuing shares. We present that the Road price-earnings ratio is superior at predicting mixture returns (each in- and out-of-sample) in addition to cross-sectional returns relative to conventional monetary ratios. Thus, it’s excellently fitted to asset pricing checks aimed toward understanding inventory value and return variation (and therefore, the surplus volatility puzzle). We additionally present that its use can reconcile conflicting views in prior analysis.

[Authors] additionally assemble a measure of “earnings earlier than particular objects” on the S&P 500 stage utilizing Compustat. Panel (A) of Determine 3 reveals that this carefully replicates the Road earnings report by I/B/E/S. “Earnings earlier than particular objects” are useful for the return prediction train since I/B/E/S started reporting realized earnings solely in 1983. We, due to this fact, use the “earnings earlier than particular objects” within the prolonged pattern beginning in 1965 (we use annual Compustat for the interval 1965 and quarterly Compustat after 1970). [. . .] Panel (C) of Determine 3 reveals a extra pronounced enhance within the PD ratio in comparison with the Road PE ratio over the previous a long time.

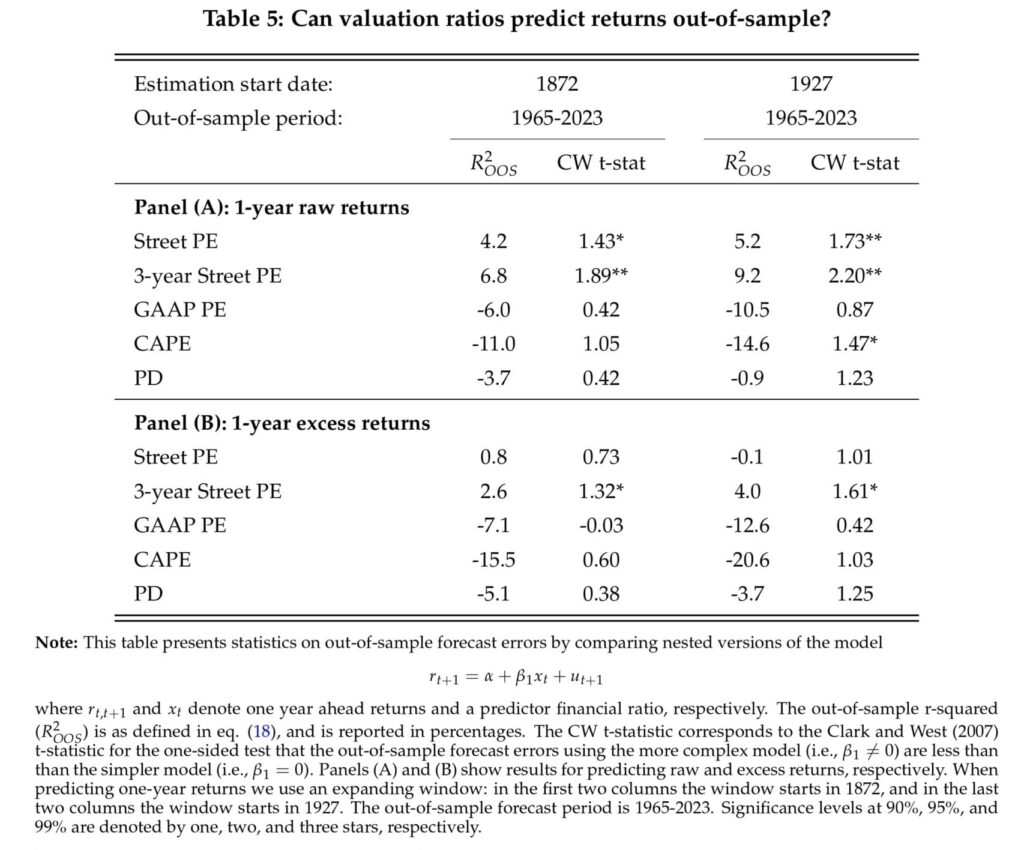

Desk 5 experiences the outcomes the place we report each R2OOS statistic and the CW t-statistic for the null that Clark-West SPE Distinction is zero towards the choice that its constructive (i.e., the extra complicated mannequin adjusted for noise performs higher). Panel (A) demonstrates that the Road PE and 3-year Road PE ratio have vital predictive energy, with R2OOS values of 4.2% and 6.8%, respectively, for the 1872 estimation begin date, and 5.2% and 9.2% for the 1927 begin date. The corresponding CW t-statistic affirm the importance of those outcomes: all the outcomes are vital on the 5% stage with the only real exception of Road PE for the 1872 estimation begin, which continues to be vital on the 10% stage. This means that these two Road-based valuation ratios are strong predictors of future returns out-of-sample. [. . .] Panel (B) of Desk 5 additionally experiences the outcomes for one-year extra returns as in Goyal and Welch (2008). The outcomes are much less favorable. Nonetheless, the Road PE and 3-year Road PE nonetheless handle to outperform the opposite valuation measures.”

Are you searching for extra methods to examine? Join our publication or go to our Weblog or Screener.

Do you need to be taught extra about Quantpedia Premium service? Verify how Quantpedia works, our mission and Premium pricing provide.

Do you need to be taught extra about Quantpedia Professional service? Verify its description, watch movies, assessment reporting capabilities and go to our pricing provide.

Are you searching for historic knowledge or backtesting platforms? Verify our record of Algo Buying and selling Reductions.

Or observe us on:

Fb Group, Fb Web page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookSeek advice from a good friend